Tue, Jun 23, 2026

[Archive]

Volume 5, Issue 1 (Feb 2020)

JNFS 2020, 5(1): 85-92 |

Back to browse issues page

Download citation:

BibTeX | RIS | EndNote | Medlars | ProCite | Reference Manager | RefWorks

Send citation to:

BibTeX | RIS | EndNote | Medlars | ProCite | Reference Manager | RefWorks

Send citation to:

Eslami M R, Baghestany A A. Modeling the Impact of Inflation Uncertainty on Food Sector Growth. JNFS 2020; 5 (1) :85-92

URL: http://jnfs.ssu.ac.ir/article-1-204-en.html

URL: http://jnfs.ssu.ac.ir/article-1-204-en.html

Agricultural Planning, Economic and Rural Development Research Institute. Tehran, Iran.

Full-Text [PDF 646 kb]

(842 Downloads)

| Abstract (HTML) (3966 Views)

Mohammad Reza Eslami; PhD1 & Ali Akbar Baghestany; PhD*2

1 Department of Agriculture and Natural Resource, School of Agricultural Management, Islamic Azad University of Yazd, Yazd, Iran.

2 Agricultural Planning, Economic and Rural Development Research Institute. Tehran, Iran.

Introduction

Economic Theory:Various economic theories make predictions about the association between the inflation volatilities and output on the one hand and the effects of these uncertainties on levels of the respective variables on the other hand. For example, a trade-of exists between the nominal uncertainty inflation and real output variability (Fuhrer, 1997). Models with a stable inflation-unemployment trade-of imply a positive relationship between nominal and real uncertainty (Logue and Sweeney, 1981). Another significant contribution concerning the relationship between inflation and inflation uncertainty was provided by other researchers (Pourgerami and Maskus, 1987). They demonstrated a negative relationship between inflation and inflation uncertainty by rejecting the harmful effect of high inflation on predictability of prices. Against the Friedman-Ball Hypothesis, they argued that higher inflation led economic agents to invest more in generating accurate predictions, which reduced their prediction error. In the literature, the mechanism of relationship from higher inflation rate to lower inflation uncertainty was called “Pourgerami and Maskus Hypothesis" (Karahan, 2012). The aggregate supply-aggregate demand (AS-AD) framework also postulated a positive relationship between inflation and growth; increase of growth increased inflation. In the 1970s, however, the concept of stagflation gained prominence and the validity of the positive relationship was questioned.

Method description: This paper employed bivariate GARCH models to estimate the conditional means of inflation and agricultural growth. In these models, and denote the inflation rate and real output growth, respectively. The residual vector is defined as Regarding , we assume that it is conditionally normal with mean vector 0 and variance covariance matrix . In which, vech . That is, where, is the information set up to time t −1. In our empirical study, we estimate several bivariate GARCH specifications for inflation and output growth. The BEKK representation for is parameterized as what has done with (Fountas and Karanasos, 2006).

Following Engle & Kroner, the GARCH BEKK model is derived as follows:

First, by defining the vector of residuals as εt and the information set at time t-1 as ωt-1, we can assume In other words, this means that the residuals were distributed conditionally normal with mean of zero and variance (covariance) matrix Ht.

Under these assumptions, the conditional variance-covariance matrix for GARCH BEKK (p, q) can be written as

.PNG)

In the case of BEKK GARCH (1, 1), this can also be written as

References

Andreou E, Pelloni A & Sensier M 2008. Is Volatility Good for Growth? Evidence from the G7. The University of Manchester, Centre for Growth and Business Cycle Research, Discussion Paper 97.

Black F 1987. Business Cycles and Equilibrium. Basil Blackwell, New York.

Blackburn K & Pelloni A 2005. Growth, cycles, and stabilization policy. Oxford economic papers. 57 (2): 262-282.

Brunner D 1993. Comment on Inflation Regimes and the Sources of Inflation Uncertainty. Journal of money, credit and banking. 25 (3): 512-520.

Bruno M & Easterly W 1995. Inflation crises and long-run growth. National Bureau of Economic Research.

Burdekin RC, Denzau AT, Keil MW, Sitthiyot T & Willett TD 2004. When does inflation hurt economic growth? Different nonlinearities for different economies. Journal of macroeconomics. 26 (3): 519-532.

Conrad C & Karanasos M 2008. Modeling volatility spillovers between the variabilities of US inflation and output: the UECCC GARCH model. University of Heidelberg Department of Economics Discussion Paper, (475).

Coulson NE & Robins RP 1985. A comment on the testing of functional form in first difference models. Review of economics and statistics. 710-712.

Fischer S 1993. The role of macroeconomic factors in growth. Journal of monetary economics. 32 (3): 485-512.

Fountas S & Karanasos M 2006. The relationship between economic growth and real uncertainty in the G3. Economic modelling. 23 (4): 638-647.

Fountas S, Karanasos M & Kim J 2002. Inflation and output growth uncertainty and their relationship with inflation and output growth. Economics letters. 75 (3): 293-301.

Freebairn JW 1981. Assessing some effects of inflation on the agricultural sector. Australian journal of agricultural economics. 25 (2): 107-122.

Friedman M 1977. Nobel lecture: inflation and unemployment. Journal of political economy. 85 (3): 451-472.

Fuhrer JC 1997. Inflation/output variance trade-offs and optimal monetary policy. Journal of money, credit, and banking. 214-234.

Grier KB, Henry ÓT, Olekalns N & Shields K 2004. The asymmetric effects of uncertainty on inflation and output growth. Journal of applied econometrics. 19 (5): 551-565.

Grier KB & Perry MJ 2000. The effects of real and nominal uncertainty on inflation and output growth: some garch‐m evidence. Journal of applied econometrics. 15 (1): 45-58.

Grier R & Grier KB 2006. On the real effects of inflation and inflation uncertainty in Mexico. Journal of development economics. 80 (2): 478-500.

jansen D 1989. Does inflation uncertainty affect output growth? Further evidence. Federal reserve bank of St. Louis Review. 43-54.

Karahan Ö 2012. The relationship between inflation and inflation uncertainty: evidence from the Turkish economy. Procedia economics and finance. 1: 219-228.

Khan MS & Ssnhadji AS 2001. Threshold effects in the relationship between inflation and growth. IMF Staff papers. 48 (1): 1-21.

Logue DE & Sweeney RJ 1981. Inflation and real growth: Some empirical results: Note. Journal of money, credit and banking. 13 (4): 497-501.

Olatunji G, Omotesho O, Ayinde O & Adewumi M 2012. Empirical Analysis Of Agricultural Production And Inflation Rate In Nigeria (1970-2006). Agrosearch. 12 (1): 21-30.

Pindyck RS 1990. Irreversibility, uncertainty, and investment. National Bureau of Economic Research.

Pishbahar E, Ghahramanzadeh M & Farhadi A 2015. The effects of inflation on production and growth of Iranian economy with emphasis on the agricultural sector. Agricultural economics. 9 (1): 19-41.

Pourgerami A & Maskus KE 1987. The effects of inflation on the predictability of price changes in Latin America: some estimates and policy implications. World development. 15 (2): 287-290.

Ramey G & Ramey VA 1991. Technology commitment and the cost of economic fluctuations. National Bureau of Economic Research.

Sandmo A 1970. The effect of uncertainty on saving decisions. The review of economic studies. 37 (3): 353-360.

Sarel M 1996. Nonlinear effects of inflation on economic growth. Staff Papers. 43 (1): 199-215.

Taylor JB 1979. Estimation and control of a macroeconomic model with rational expectations. Econometrica: Journal of the econometric society. 1267-1286.

Full-Text: (1042 Views)

Modeling the Impact of Inflation Uncertainty on Food Sector Growth

Mohammad Reza Eslami; PhD1 & Ali Akbar Baghestany; PhD*2

1 Department of Agriculture and Natural Resource, School of Agricultural Management, Islamic Azad University of Yazd, Yazd, Iran.

2 Agricultural Planning, Economic and Rural Development Research Institute. Tehran, Iran.

| ARTICLE INFO | ABSTRACT | |

| ORIGINAL ARTICLE | Background: One of the most fundamental objectives of the macroeconomic policies is to realize the relationship between economic growth and inflation. According to some monetary policy advisors, inflation reflects erosion in consumer’s purchasing power. Inflation as an important economic variable, affect the economic growth and its impact on economic growth has been proposed in various theories. Agriculture plays an important role in providing the food security in Iran. Methods: A Bivariate GARCH model was employed to investigate the relationship between inflation uncertainty and agricultural growth. Results: The Augmented Dickey Fuller and Phillips Perron tests indicated all variables were stationary. Estimated models were utilized to generate the conditional variances of inflation and agriculture growth as proxies of inflation and growth variability. During the entire period 1990-2012, Bivariate Granger Causality test indicated that inflation uncertainty was the cause of growth in agriculture. This finding was in line with the hypothesis presented by (Logue and Sweeney, 1981). Conclusion: Due to the causality relation of inflation uncertainty and growth in agriculture, macro policy decision-makers are recommended to consider the price policies for improving agricultural production. Keywords: Bivariate GARCH process; Inflation Uncertainty; Agriculture; Iran |

|

| Article history: Received: 28 Aug 2018 Revised: 3 Nov 2018 Accepted: 17 Feb2019 |

||

| *Corresponding author: a.baghestany@agri-peri.ac.ir Assistant professor. Agriculture and Food Policies Research Department. Agricultural Planning, Economic and Rural Development Research Institute. Tehran, Iran. Postal code: 15986-37313 Tel: +98 21 42916000 |

Introduction

The effect of inflation on economic performance has been an important and complex topic in the literature, because if systematic inflation has real effects, governments can influence economic performance through monetary policy. Little theoretical consensus exists on the way that inflation affects economic performance. Much of the empirical literature indicated a negative influence of inflation on growth. However, many economic theories predict a neutral or even positive effect of average inflation on economic performance. Apart from the effect of trend inflation, inflation uncertainty may also influence the output growth. As in the case of average inflation, the effect of uncertainty on growth can either be positive or negative (Grier and Grier, 2006, Olatunji et al., 2012).

In discussing the effects of inflation on the agricultural sector, it is worth noting that agriculture involves a number of interdependent activities. In other words, it is highly integrated with and affected by the rest of the economy and depends on export markets for a large proportion of sales and to a lesser extent on imported inputs. It is also dependent on resource use and institutional peculiarities that influence prices and incomes. The modern agricultural sector consists of a number of highly specialized industries in which goods pass through a number of intermediate stages before reaching the final consumer. Several industries provide a diversity of items including capital equipment (e.g., tractors and buildings), material inputs (e.g., fertilizer and fuel), and services (e.g., accountancy advice and marketing services) for farmers' use. These purchased inputs, along with land and associated resources, labor, and management are combined by farmers to produce farm products (e.g., wheat, wool, and animals). Farm products pass through a number of processes before reaching final consumers in the desired form, time, and place (Freebairn, 1981).

Some researchers found a positive association between this measure of inflation uncertainty and US economic performance (Coulson and Robins, 1985), while some others found no significant relationship in this regard (jansen, 1989). A negative relationship was reported between inflation uncertainty and growth in the US (Grier et al., 2004, Grier and Perry, 2000) . Bivariate GARCH models were used to simultaneously estimate the conditional means, variances, and covariance of inflation and output growth (Grier et al., 2004, Grier and Perry, 2000). Some studies found that the effect of inflation on output growth varies with the level of inflation (Bruno and Easterly, 1995, Burdekin et al., 2004, Fischer, 1993, Khan and Ssnhadji, 2001, Sarel, 1996). A bivariate GARCH model of inflation and output growth was also applied by some other researchers (Fountas et al., 2002). The literature showed that the relationship between inflation and growth was different in various economies. In Iran, due to the high inflation rate, the response of each economic sector to this inflation is different. Considering the importance of agricultural role in the economy of Iran, the effect of inflation on agricultural growth was investigated since it consequently affects the welfare of the rural population. Therefore, this paper for the first time, is modelled inflation uncertainty (by using Bivariate GARCH models that take in to consideration prices variables variance Heteroskedasticity) and investigate the effect and the relationship between inflation uncertainty and growth volatility in Iranian agriculture. The purpose of this study is to determine the direction and the amount of impression between these two macro-economic variables which could be a good fingerpost and guideline for policy makers.

Material and Methods

Data on inflation and agricultural growth of Iran during 1990-2016 provided from the Statistical Office, Central Bank of Iran:

Some researchers found a positive association between this measure of inflation uncertainty and US economic performance (Coulson and Robins, 1985), while some others found no significant relationship in this regard (jansen, 1989). A negative relationship was reported between inflation uncertainty and growth in the US (Grier et al., 2004, Grier and Perry, 2000) . Bivariate GARCH models were used to simultaneously estimate the conditional means, variances, and covariance of inflation and output growth (Grier et al., 2004, Grier and Perry, 2000). Some studies found that the effect of inflation on output growth varies with the level of inflation (Bruno and Easterly, 1995, Burdekin et al., 2004, Fischer, 1993, Khan and Ssnhadji, 2001, Sarel, 1996). A bivariate GARCH model of inflation and output growth was also applied by some other researchers (Fountas et al., 2002). The literature showed that the relationship between inflation and growth was different in various economies. In Iran, due to the high inflation rate, the response of each economic sector to this inflation is different. Considering the importance of agricultural role in the economy of Iran, the effect of inflation on agricultural growth was investigated since it consequently affects the welfare of the rural population. Therefore, this paper for the first time, is modelled inflation uncertainty (by using Bivariate GARCH models that take in to consideration prices variables variance Heteroskedasticity) and investigate the effect and the relationship between inflation uncertainty and growth volatility in Iranian agriculture. The purpose of this study is to determine the direction and the amount of impression between these two macro-economic variables which could be a good fingerpost and guideline for policy makers.

Material and Methods

Data on inflation and agricultural growth of Iran during 1990-2016 provided from the Statistical Office, Central Bank of Iran:

- Producer price index(PPI) in Iran in constant price 2011 = 100

- Agricultural value added in Billion Rials in constant price 2011 = 100

Economic Theory:Various economic theories make predictions about the association between the inflation volatilities and output on the one hand and the effects of these uncertainties on levels of the respective variables on the other hand. For example, a trade-of exists between the nominal uncertainty inflation and real output variability (Fuhrer, 1997). Models with a stable inflation-unemployment trade-of imply a positive relationship between nominal and real uncertainty (Logue and Sweeney, 1981). Another significant contribution concerning the relationship between inflation and inflation uncertainty was provided by other researchers (Pourgerami and Maskus, 1987). They demonstrated a negative relationship between inflation and inflation uncertainty by rejecting the harmful effect of high inflation on predictability of prices. Against the Friedman-Ball Hypothesis, they argued that higher inflation led economic agents to invest more in generating accurate predictions, which reduced their prediction error. In the literature, the mechanism of relationship from higher inflation rate to lower inflation uncertainty was called “Pourgerami and Maskus Hypothesis" (Karahan, 2012). The aggregate supply-aggregate demand (AS-AD) framework also postulated a positive relationship between inflation and growth; increase of growth increased inflation. In the 1970s, however, the concept of stagflation gained prominence and the validity of the positive relationship was questioned.

Method description: This paper employed bivariate GARCH models to estimate the conditional means of inflation and agricultural growth. In these models, and denote the inflation rate and real output growth, respectively. The residual vector is defined as Regarding , we assume that it is conditionally normal with mean vector 0 and variance covariance matrix . In which, vech . That is, where, is the information set up to time t −1. In our empirical study, we estimate several bivariate GARCH specifications for inflation and output growth. The BEKK representation for is parameterized as what has done with (Fountas and Karanasos, 2006).

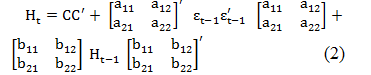

Following Engle & Kroner, the GARCH BEKK model is derived as follows:

First, by defining the vector of residuals as εt and the information set at time t-1 as ωt-1, we can assume In other words, this means that the residuals were distributed conditionally normal with mean of zero and variance (covariance) matrix Ht.

Under these assumptions, the conditional variance-covariance matrix for GARCH BEKK (p, q) can be written as

In the case of BEKK GARCH (1, 1), this can also be written as

The most important feature of the GARCH BEKK specification is the non-negativity of conditional variance-covariance matrix. This is guaranteed by the pairing of each matrix (A, B, and C) with their transpose.

Agricultural value added trend: Figure 1 shows that agricultural value added relatively increased during 2004-2016. The reasons for this would be increasing demand for food due to population growth so, food supply and production increased. However, in 2008, due to lower investment and inappropriate weather condition, a reduction occurred in agriculture value added.

Figure 2 shows the relationship between PPI and agricultural value added (AVA). This figure illustrates a positive but nonlinear relationship between these two variables.

Results

In our empirical analysis, we used PPI and AVA as proxies for the price level and output, respectively. The data had annual frequency and ranged from 1990 to 2012. Inflation was measured by the difference of the log PPI, and agricultural output growth was measured by the difference in the log of the AVA.

First, we tested whether the time series variables were stationary I (1) or not. We considered 2 different tests: first, the Augmented Dickey Fuller (ADF) test with the lag length determined by the AIC criterion and second, the Phillips–Perron test. These tests were non-stationary as their null hypothesis. Table 1 presents the results of stationary tests for inflation and Agricultural output growth. Considering the inflation and agricultural output growth, the null hypothesis of a unit root was reject at the 0.1 level using the ADF test and Phillips–Perron test. Thus, we concluded that the inflation rate and agricultural growth were stationary.

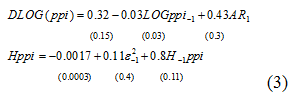

Equations 3 and 4 report estimated of the Bivariate GARCH model. The conditional variance equation for inflation and agricultural output were also reported. The GARCH parameters were significant at the 0.01 level. The sum of the parameters ( ) was 0.9 in Equation 3 (Hppi) and also this sum is equal to 1 in Equation 4 (Hava) which showed that this regression was real. In other words, the past information remained important for the predictions of the conditional variances for long horizons with regard to the output growth.

.PNG)

Results of Equation 3 indicated inflation uncertainty with one lag has a positive and significant impact on its current variable (0.8). The covariance coefficient in Equation 4 (1.17) was positive which showed that inflation uncertainty had a positive impact on output growth (Logue and Sweeney, 1981). This result is in line with the results of other researchers (Pishbahar et al., 2015) reporting a positive relationship between Iran's inflation and agricultural output growth.

Next, we reported the results of Granger-causality tests to provide some statistical evidence on the nature of the relationship between inflation uncertainty and output growth. Table 2 presented the F statistics of Granger-causality tests. The first row in Table 2 considered the granger causality from inflation and agricultural output growth to uncertainty inflation and agricultural output growth.

.PNG)

.PNG)

.PNG)

Agricultural value added trend: Figure 1 shows that agricultural value added relatively increased during 2004-2016. The reasons for this would be increasing demand for food due to population growth so, food supply and production increased. However, in 2008, due to lower investment and inappropriate weather condition, a reduction occurred in agriculture value added.

Figure 2 shows the relationship between PPI and agricultural value added (AVA). This figure illustrates a positive but nonlinear relationship between these two variables.

Results

In our empirical analysis, we used PPI and AVA as proxies for the price level and output, respectively. The data had annual frequency and ranged from 1990 to 2012. Inflation was measured by the difference of the log PPI, and agricultural output growth was measured by the difference in the log of the AVA.

First, we tested whether the time series variables were stationary I (1) or not. We considered 2 different tests: first, the Augmented Dickey Fuller (ADF) test with the lag length determined by the AIC criterion and second, the Phillips–Perron test. These tests were non-stationary as their null hypothesis. Table 1 presents the results of stationary tests for inflation and Agricultural output growth. Considering the inflation and agricultural output growth, the null hypothesis of a unit root was reject at the 0.1 level using the ADF test and Phillips–Perron test. Thus, we concluded that the inflation rate and agricultural growth were stationary.

Equations 3 and 4 report estimated of the Bivariate GARCH model. The conditional variance equation for inflation and agricultural output were also reported. The GARCH parameters were significant at the 0.01 level. The sum of the parameters ( ) was 0.9 in Equation 3 (Hppi) and also this sum is equal to 1 in Equation 4 (Hava) which showed that this regression was real. In other words, the past information remained important for the predictions of the conditional variances for long horizons with regard to the output growth.

Results of Equation 3 indicated inflation uncertainty with one lag has a positive and significant impact on its current variable (0.8). The covariance coefficient in Equation 4 (1.17) was positive which showed that inflation uncertainty had a positive impact on output growth (Logue and Sweeney, 1981). This result is in line with the results of other researchers (Pishbahar et al., 2015) reporting a positive relationship between Iran's inflation and agricultural output growth.

Next, we reported the results of Granger-causality tests to provide some statistical evidence on the nature of the relationship between inflation uncertainty and output growth. Table 2 presented the F statistics of Granger-causality tests. The first row in Table 2 considered the granger causality from inflation and agricultural output growth to uncertainty inflation and agricultural output growth.

Discussion

We found strong evidences that increased inflation reduced inflation uncertainty, confirming the theoretical predictions of (Pourgerami and Maskus, 1987). Furthermore, the null hypothesis of "There is not a Granger causality relation from output growth to output growth uncertainty" was rejected at the 1% level of significance. The association between the two variables were negative, which is in line with the predictions of some other researchers (Fountas and Karanasos, 2006). The second row in Table 2 provides evidences that inflation uncertainty did not cause agricultural output growth, which rejected the null hypotheses at the 5% level of significance. Hence, our key result was that inflation uncertainty increased real agricultural output growth. So, we provided strong empirical support for Dostey and Sarte hypotheses. In summary, our results showed that higher inflation uncertainty and more inflation increased agricultural output growth in the economy of Iran.

Therefore, based on equation 4, inflation uncertainty significantly increased real out put growth to 1.17% in the short run, which provided strong empirical support of the reuslts found by (Logue and Sweeney, 1981). Iran has a supportive economic, in which different sectors are supported by government supportive policies. So, during the high inflation fluctuations and high price fluctuations, people prefer to decrease their savings and increase their cash. Since Iran is classified as a low income country, households are more intended to consume essential goods than luxieries during high inflation uncertainity. Therefore, demand for eatable goods and agricultural products increases. On the one hand, the supply of agriculture sector or agriculture products increses and on the other hand, the government supports this sector with supportive policies for providing food security in society.

Conclusion

We used a Bivariate GARCH model to obtain estimates of inflation uncertainty and examine the bidirectional causal relationships between inflation uncertainty and real agricultural growth. Our evidence supported the conclusion that a higher rate of inflation uncertainty Granger causality for increase in the agricultural output growth. Since one of the main reasons for inflation in Iran is liquidity, especially in recent years. According to the Engle law, with increase in liquidity and cash money available to the public, the demand for essential goods and food increases in developing countries such as Iran. This means high demand for agricultural output. However, high inflation uncertainty increased the uncertainty in economic society. Therefore, the government should support the agricultural sector by policies such as guaranteed prices and fixed priced to avoid instability food security. In inflationary terms, while the economy is experiencing high food prices, the government would work to increase food supply by increasing its support for agriculture. Therefore, the opportunity of food accessibility provided for everyone. This may be lead to growth of agriculture as a provider of food security

Conflict of interest

There was no conflict of interest in this study.

Acknowledgment

We are thankful of Dr. Habibeh Sherafatmand who participate in this study, without her advices and help it was impossible to do this work.

Authors’ Contribution

Baghestany AA designed the study and revised the Content, scientific writing, and discussion, analyzed the data and interpreted the methods and results and Conclusion. Eslami MR contributed in conducting the study. Authors reviewed the Paper and confirmed it.

We found strong evidences that increased inflation reduced inflation uncertainty, confirming the theoretical predictions of (Pourgerami and Maskus, 1987). Furthermore, the null hypothesis of "There is not a Granger causality relation from output growth to output growth uncertainty" was rejected at the 1% level of significance. The association between the two variables were negative, which is in line with the predictions of some other researchers (Fountas and Karanasos, 2006). The second row in Table 2 provides evidences that inflation uncertainty did not cause agricultural output growth, which rejected the null hypotheses at the 5% level of significance. Hence, our key result was that inflation uncertainty increased real agricultural output growth. So, we provided strong empirical support for Dostey and Sarte hypotheses. In summary, our results showed that higher inflation uncertainty and more inflation increased agricultural output growth in the economy of Iran.

Therefore, based on equation 4, inflation uncertainty significantly increased real out put growth to 1.17% in the short run, which provided strong empirical support of the reuslts found by (Logue and Sweeney, 1981). Iran has a supportive economic, in which different sectors are supported by government supportive policies. So, during the high inflation fluctuations and high price fluctuations, people prefer to decrease their savings and increase their cash. Since Iran is classified as a low income country, households are more intended to consume essential goods than luxieries during high inflation uncertainity. Therefore, demand for eatable goods and agricultural products increases. On the one hand, the supply of agriculture sector or agriculture products increses and on the other hand, the government supports this sector with supportive policies for providing food security in society.

Conclusion

We used a Bivariate GARCH model to obtain estimates of inflation uncertainty and examine the bidirectional causal relationships between inflation uncertainty and real agricultural growth. Our evidence supported the conclusion that a higher rate of inflation uncertainty Granger causality for increase in the agricultural output growth. Since one of the main reasons for inflation in Iran is liquidity, especially in recent years. According to the Engle law, with increase in liquidity and cash money available to the public, the demand for essential goods and food increases in developing countries such as Iran. This means high demand for agricultural output. However, high inflation uncertainty increased the uncertainty in economic society. Therefore, the government should support the agricultural sector by policies such as guaranteed prices and fixed priced to avoid instability food security. In inflationary terms, while the economy is experiencing high food prices, the government would work to increase food supply by increasing its support for agriculture. Therefore, the opportunity of food accessibility provided for everyone. This may be lead to growth of agriculture as a provider of food security

Conflict of interest

There was no conflict of interest in this study.

Acknowledgment

We are thankful of Dr. Habibeh Sherafatmand who participate in this study, without her advices and help it was impossible to do this work.

Authors’ Contribution

Baghestany AA designed the study and revised the Content, scientific writing, and discussion, analyzed the data and interpreted the methods and results and Conclusion. Eslami MR contributed in conducting the study. Authors reviewed the Paper and confirmed it.

References

Andreou E, Pelloni A & Sensier M 2008. Is Volatility Good for Growth? Evidence from the G7. The University of Manchester, Centre for Growth and Business Cycle Research, Discussion Paper 97.

Black F 1987. Business Cycles and Equilibrium. Basil Blackwell, New York.

Blackburn K & Pelloni A 2005. Growth, cycles, and stabilization policy. Oxford economic papers. 57 (2): 262-282.

Brunner D 1993. Comment on Inflation Regimes and the Sources of Inflation Uncertainty. Journal of money, credit and banking. 25 (3): 512-520.

Bruno M & Easterly W 1995. Inflation crises and long-run growth. National Bureau of Economic Research.

Burdekin RC, Denzau AT, Keil MW, Sitthiyot T & Willett TD 2004. When does inflation hurt economic growth? Different nonlinearities for different economies. Journal of macroeconomics. 26 (3): 519-532.

Conrad C & Karanasos M 2008. Modeling volatility spillovers between the variabilities of US inflation and output: the UECCC GARCH model. University of Heidelberg Department of Economics Discussion Paper, (475).

Coulson NE & Robins RP 1985. A comment on the testing of functional form in first difference models. Review of economics and statistics. 710-712.

Fischer S 1993. The role of macroeconomic factors in growth. Journal of monetary economics. 32 (3): 485-512.

Fountas S & Karanasos M 2006. The relationship between economic growth and real uncertainty in the G3. Economic modelling. 23 (4): 638-647.

Fountas S, Karanasos M & Kim J 2002. Inflation and output growth uncertainty and their relationship with inflation and output growth. Economics letters. 75 (3): 293-301.

Freebairn JW 1981. Assessing some effects of inflation on the agricultural sector. Australian journal of agricultural economics. 25 (2): 107-122.

Friedman M 1977. Nobel lecture: inflation and unemployment. Journal of political economy. 85 (3): 451-472.

Fuhrer JC 1997. Inflation/output variance trade-offs and optimal monetary policy. Journal of money, credit, and banking. 214-234.

Grier KB, Henry ÓT, Olekalns N & Shields K 2004. The asymmetric effects of uncertainty on inflation and output growth. Journal of applied econometrics. 19 (5): 551-565.

Grier KB & Perry MJ 2000. The effects of real and nominal uncertainty on inflation and output growth: some garch‐m evidence. Journal of applied econometrics. 15 (1): 45-58.

Grier R & Grier KB 2006. On the real effects of inflation and inflation uncertainty in Mexico. Journal of development economics. 80 (2): 478-500.

jansen D 1989. Does inflation uncertainty affect output growth? Further evidence. Federal reserve bank of St. Louis Review. 43-54.

Karahan Ö 2012. The relationship between inflation and inflation uncertainty: evidence from the Turkish economy. Procedia economics and finance. 1: 219-228.

Khan MS & Ssnhadji AS 2001. Threshold effects in the relationship between inflation and growth. IMF Staff papers. 48 (1): 1-21.

Logue DE & Sweeney RJ 1981. Inflation and real growth: Some empirical results: Note. Journal of money, credit and banking. 13 (4): 497-501.

Olatunji G, Omotesho O, Ayinde O & Adewumi M 2012. Empirical Analysis Of Agricultural Production And Inflation Rate In Nigeria (1970-2006). Agrosearch. 12 (1): 21-30.

Pindyck RS 1990. Irreversibility, uncertainty, and investment. National Bureau of Economic Research.

Pishbahar E, Ghahramanzadeh M & Farhadi A 2015. The effects of inflation on production and growth of Iranian economy with emphasis on the agricultural sector. Agricultural economics. 9 (1): 19-41.

Pourgerami A & Maskus KE 1987. The effects of inflation on the predictability of price changes in Latin America: some estimates and policy implications. World development. 15 (2): 287-290.

Ramey G & Ramey VA 1991. Technology commitment and the cost of economic fluctuations. National Bureau of Economic Research.

Sandmo A 1970. The effect of uncertainty on saving decisions. The review of economic studies. 37 (3): 353-360.

Sarel M 1996. Nonlinear effects of inflation on economic growth. Staff Papers. 43 (1): 199-215.

Taylor JB 1979. Estimation and control of a macroeconomic model with rational expectations. Econometrica: Journal of the econometric society. 1267-1286.

Type of article: review article |

Subject:

public specific

Received: 2018/08/28 | Published: 2020/02/1 | ePublished: 2020/02/1

Received: 2018/08/28 | Published: 2020/02/1 | ePublished: 2020/02/1

References

1. Andreou E, Pelloni A & Sensier M 2008. Is Volatility Good for Growth? Evidence from the G7. The University of Manchester, Centre for Growth and Business Cycle Research, Discussion Paper 97.

2. Black F 1987. Business Cycles and Equilibrium. Basil Blackwell, New York.

3. Blackburn K & Pelloni A 2005. Growth, cycles, and stabilization policy. Oxford economic papers. 57 (2): 262-282.

4. Brunner D 1993. Comment on Inflation Regimes and the Sources of Inflation Uncertainty. Journal of money, credit and banking. 25 (3): 512-520.

5. Bruno M & Easterly W 1995. Inflation crises and long-run growth. National Bureau of Economic Research.

6. Burdekin RC, Denzau AT, Keil MW, Sitthiyot T & Willett TD 2004. When does inflation hurt economic growth? Different nonlinearities for different economies. Journal of macroeconomics. 26 (3): 519-532.

7. Conrad C & Karanasos M 2008. Modeling volatility spillovers between the variabilities of US inflation and output: the UECCC GARCH model. University of Heidelberg Department of Economics Discussion Paper, (475).

8. Coulson NE & Robins RP 1985. A comment on the testing of functional form in first difference models. Review of economics and statistics. 710-712.

9. Fischer S 1993. The role of macroeconomic factors in growth. Journal of monetary economics. 32 (3): 485-512.

10. Fountas S & Karanasos M 2006. The relationship between economic growth and real uncertainty in the G3. Economic modelling. 23 (4): 638-647.

11. Fountas S, Karanasos M & Kim J 2002. Inflation and output growth uncertainty and their relationship with inflation and output growth. Economics letters. 75 (3): 293-301.

12. Freebairn JW 1981. Assessing some effects of inflation on the agricultural sector. Australian journal of agricultural economics. 25 (2): 107-122.

13. Friedman M 1977. Nobel lecture: inflation and unemployment. Journal of political economy. 85 (3): 451-472.

14. Fuhrer JC 1997. Inflation/output variance trade-offs and optimal monetary policy. Journal of money, credit, and banking. 214-234.

15. Grier KB, Henry ÓT, Olekalns N & Shields K 2004. The asymmetric effects of uncertainty on inflation and output growth. Journal of applied econometrics. 19 (5): 551-565.

16. Grier KB & Perry MJ 2000. The effects of real and nominal uncertainty on inflation and output growth: some garch‐m evidence. Journal of applied econometrics. 15 (1): 45-58.

17. Grier R & Grier KB 2006. On the real effects of inflation and inflation uncertainty in Mexico. Journal of development economics. 80 (2): 478-500.

18. jansen D 1989. Does inflation uncertainty affect output growth? Further evidence. Federal reserve bank of St. Louis Review. 43-54.

19. Karahan Ö 2012. The relationship between inflation and inflation uncertainty: evidence from the Turkish economy. Procedia economics and finance. 1: 219-228.

20. Khan MS & Ssnhadji AS 2001. Threshold effects in the relationship between inflation and growth. IMF Staff papers. 48 (1): 1-21.

21. Logue DE & Sweeney RJ 1981. Inflation and real growth: Some empirical results: Note. Journal of money, credit and banking. 13 (4): 497-501.

22. Olatunji G, Omotesho O, Ayinde O & Adewumi M 2012. Empirical Analysis Of Agricultural Production And Inflation Rate In Nigeria (1970-2006). Agrosearch. 12 (1): 21-30.

23. Pindyck RS 1990. Irreversibility, uncertainty, and investment. National Bureau of Economic Research.

24. Pishbahar E, Ghahramanzadeh M & Farhadi A 2015. The effects of inflation on production and growth of Iranian economy with emphasis on the agricultural sector. Agricultural economics. 9 (1): 19-41.

25. Pourgerami A & Maskus KE 1987. The effects of inflation on the predictability of price changes in Latin America: some estimates and policy implications. World development. 15 (2): 287-290.

26. Ramey G & Ramey VA 1991. Technology commitment and the cost of economic fluctuations. National Bureau of Economic Research.

27. Sandmo A 1970. The effect of uncertainty on saving decisions. The review of economic studies. 37 (3): 353-360.

28. Sarel M 1996. Nonlinear effects of inflation on economic growth. Staff Papers. 43 (1): 199-215.

29. Taylor JB 1979. Estimation and control of a macroeconomic model with rational expectations. Econometrica: Journal of the econometric society. 1267-1286.

| Rights and permissions | |

|

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License. |